I know anyone who has studied moral ethics smells something fishy in the banking and loans system of the United States. I remember studying finance in Undergrad and just being baffled by the system. I couldn’t understand why loans were amortized the way they taught us in school. I was so confused, I even attempted to write a twenty page paper about it. What I could never understand is, “Why give high interest rates to high risk borrowers?”

The textbook answer is a tenant of Capitalism, “High risk means High reward.” The logic is because the borrowers are “High Risk” then the banks deserve higher compensation for the risk of lending to a high risk borrower. On the surface, it makes sense, but if you dive deeper, then it really doesn’t.

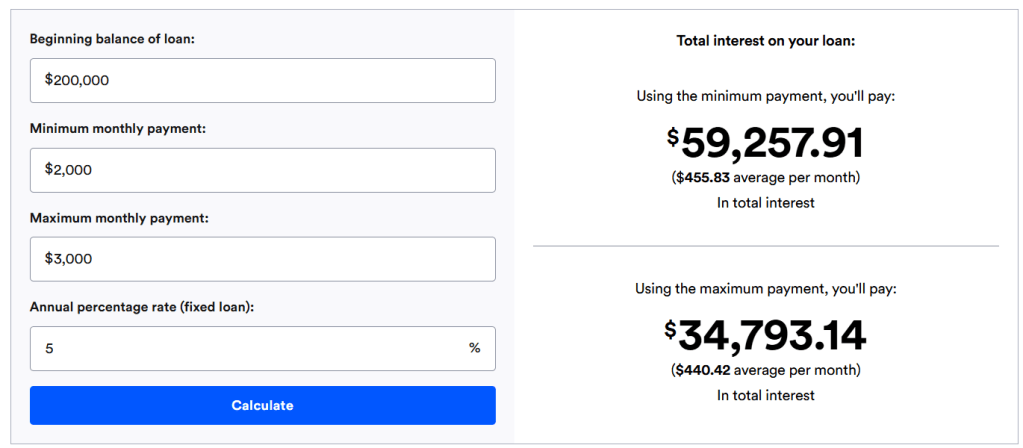

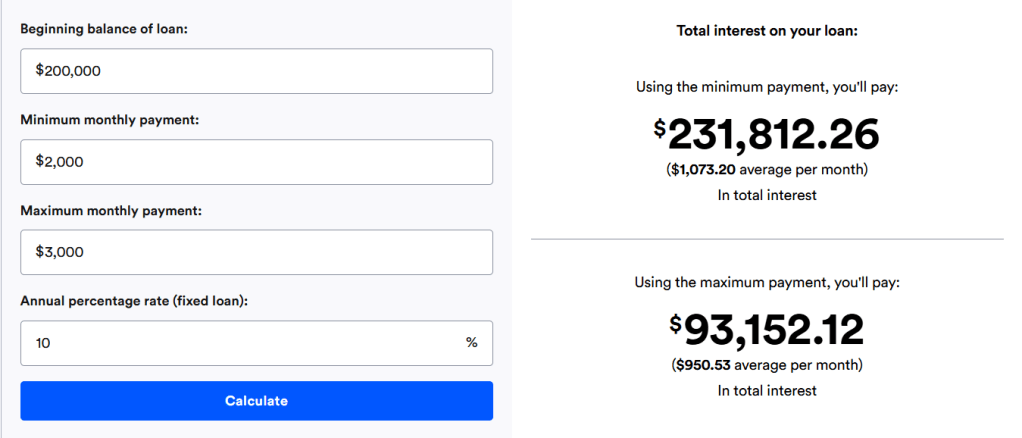

We have a high risk borrower and a low risk borrower. Let us call the high risk borrower “Gimme S’more” and the low risk borrower “Rich McGee.” Gimme and Rich submit their loan application for a house. They want the same house that’s valued at $200k. They get a fixed rate installment loan so it’ll last as long as it takes to pay off the loan. They both get approved! They have a minimum payment of $2000 and a maximum payment of $3000. However, Gimme has a 10% interest rate and Rich has a 5% interest rate. (Thank you Bankrate.com for your loan calculator!)

The Difference is almost scandalous! Of course, actual loan amounts may vary according to market rates and terms of the loan. Still, high risk borrowers often pay significantly more than low risk borrowers. In extreme cases, borrowers could pay multiple of the principal amount. In our example, Gimme is spending $231,812 just in interest! That is more than the original principal! Meanwhile, Rich McGee is only paying $59,257 in interest. Rich McGee is able to pay off his loan months ahead of Gimme S’more

The only way for Gimme S’more to save money on interest is by increasing their monthly payments. Our example above has the two borrowers use the same payments. Let us change the example so Gimme has a higher monthly payment.

We see with a payment of $2000, Gimme would need to pay $231,812.26. With a payment of $3000, Gimme would need to pay 93,152.12. With a payment of $5000, Gimme would need to pay $44,293.85. May God have mercy on Gimme S’more if the bank suggested to only pay the minimum of $2000. Such crippling debt ought to be considered usurious!

We see something curious with this higher payment as well. Look at how much interest Rich McGee is paying in comparison to Gimme’s higher payment. With a payment of $2000, Rich McGee is paying 59,257.91 in interest. With a payment of $5000, Gimme S’more is paying 44,293.83 in interest. Gimme S’more has to pay twice the amount in monthly payments in order to payout the same amount of interest to the banks as Rich McGee.

Here is the irony of the high risk borrower. In theory, these loan agreements are made in advance to the payments. The risk the bank takes is if the borrower is able to pay their share of the loan. Low risk borrowers are considered more trustworthy so they have easier terms, because the bank doesn’t have to be compensated as much for the risk. The High risk borrowers are considered to be more risky and therefore the bank asks for higher payments to compensate them for the risk.

Do you see the irony yet? The high risk borrower agrees to stricter terms or higher payments at the beginning of the loan. On one hand, they could just agree to a bad deal because they have no other option available to them. On the other hand, they could agree to the deal because they have the confidence that they could afford the payments. Let me repeat that, THEY HAVE CONFIDENCE THAT THEY COULD AFFORD THE PAYMENTS.

The burden of payment is vastly greater on the high risk borrower than the low risk borrower. Gimme S’more pays more in interest than Rich McGee, unless Gimme pays a monthly payment that is more than double. That means that Gimme S’more has the confidence that they are able to perform in such a way that they could outpace Rich McGee monthly payment by over 100%. If I had to place my trust between someone who only promises $2000 a month over someone who promises $5000, then I’d say the one who delivers $5000 is the better business.

Now, in defense of the banks, the banks are not guarantee either Rich McGee or Gimme S’more will have success. Which is why collateral is an important negotiation tool for both the banks and borrowers. Gimme S’more could promise $5000 a month and default within a year of the loan. Then, Gimme S’more declares bankruptcy and the banks are out $200,000 with no hope of getting a penny back.

The irony is that high loan payments can be a reason a business can’t keep up with expenses. The irony is that the bank is trusting the high risk borrower to perform extremely well. The irony is that low risk borrower has less stressors than the high risk borrower.

This system never made sense to me in undergrad. I couldn’t understand how it could be good business to give high risk borrowers stricter loan deals. I would think that if the bank wants their money back, that the banks would create loan terms that favors the borrower. If the bank expects Gimme S’more to pay a %10 interest rate successfully, then wouldn’t that automatically qualify Gimme S’more the lower interest rate? If Gimme could afford a %10 rate, then he can easily afford a 5%. That’s the irony that I couldn’t get pass. Some people are skeptical if he could afford a 5% rate, then why does it make sense to charge him a 10% interest rate! Do you see the irony that drove me crazy in my finance classes?

I understand banks need to perform risk mitigation strategies. To me, it would make sense to change the length of the loan more than the interest rate. We have a high risk borrower and a low risk borrower. My logic would be that I do not trust the high risk borrower. So, I want the money back as soon as possible since I lack trust in his ability to pay it back. For the low risk borrower, I am willing to wait longer, because I can trust his ability to pay it back.

In this way, Rich McGee and Gimme S’more would have the same loan terms. The only difference would be how much they are expected to pay back. Say they both got the %10 interest rate, but were expected to pay different monthly payments: Rich McGee at $3000 and Gimme S’more at $5000. The risk mitigation would come from the length of the loan and not the interest rate. The shorter the loan the less interest is paid. The longer the loan then the more interest is paid. The high risk borrower is expected to pay less in interest, because they are considered to be a bad investment. The low risk borrower is expected to pay more in interest, because they are considered to be a good investment. We see here the profit incentives are in a healthier alignment than using the interest rates. With the current system of using interest rates, the profit incentives is to find risky borrowers and keep them in perpetual debt.

On the new payment plans that I suggest, the two risk profiles can predictably adjust their payment strategies. Rich McGee is going to increase his payment to lower his interest payment as much as possible. Gimme S’more is going to find ways to pay less than $5000 dollars which leads to a higher interest payment. We see the payment on interest is reflected by the risk level of the borrower. The low risk borrower will act in a way that pays less in interest, and the high risk borrower will act in a way that pays more in interest. This organic behavior is reflective of the principle “higher risk means higher rewards.”

I could never understand how the banking system amortized loans. Perhaps, I am ignorant and am missing a key piece of information. But on a philosophical understanding, the process doesn’t make sense. There seems to be an incentive that higher risk loans profits pay off low risk loans or default loans. It doesn’t make sense to me to rely on high risk borrowers for profits.

If you know better than me, then comment below. Because I simply don’t understand why high interest rates for high risk borrowers is the best risk mitigation tool.

Leave a comment